Term life insurance is one of the most popular types of life insurance. It works very differently from another type called whole life insurance and comes with its own advantages and disadvantages. Many people choose this type of insurance to protect their loved ones after they pass away. However, term life may not be right for everyone interested in life insurance. Some people prefer the benefits of whole life policies, while others find that term life better suits their needs. To learn more about term life insurance, contact Wenatchee Insurance Agency in Wenatchee, WA.

A Set Period

Term life insurance gets its name from the set term of time during which the policy remains active. These policies have a specific expiration date, which can range from 10 to 25 years, among other options. Once that term has passed and the policyholder is still alive, the policy expires. At that point, the policyholder would need to purchase a new policy to maintain coverage. The trade-off is that term life policies are highly budget-friendly and more affordable for many people who may not be able to afford a whole life policy.

The Death Benefit

Term life insurance functions similarly to other types of life insurance, as it pays a death benefit to beneficiaries upon the policyholder’s passing. This is the primary purpose of life insurance, as it provides financial support for loved ones left behind. The amount of the death benefit is determined at the time the policy is written. Generally, higher coverage amounts are accompanied by higher premiums.

Get Life Insurance in Wenatchee

If you don’t have life insurance, now is the time to get a policy to protect your loved ones. To get started with a policy of your own, contact Wenatchee Insurance Agency in Wenatchee, WA today.

Since Wenatchee Insurance is located in the Apple Capital of the World, we do our best to meet the Orchards and small businesses in our area. One of the ways that we are able to is by visiting their fruit stand during harvest. We do our best to carry cash to lower transaction fees. If you want fresh fruits & vegetables while putting money directly into farmers hands then this is one of the best ways to do it.

While there are some very large tourist driven stands, we have been doing our best to visit the smaller operations. Some of these we have been visiting 20 plus years while others it has been our first stop. We are doing farm house rules by purchasing something fresh and something preserved.

Eagle Rock Fruit Stand: address 4911 Selfs Motel Rd, Cashmere, WA 98815 : Phone: (509) 470-6292 Facebook Page; Just did their 20th Anniversary. One of the most affordable that we found for cherries.

The Peachman (formerly Tonz Ochards): address is 4820 Cascade Ln, East Wenatchee, WA 98802: Phone (509) 630-4674 Facebook Page One of the few places where we were able to find Pie Cherries. They had a great selection of pickled goods. We pulled a bottle of Peach syrup out of here.

Miller Orchards: address is 7306 US-97, Peshastin, WA 98847 : phone (509) 669-3784 Facebook Page Yes, this is where Matt can find his Santini Cherries. They have very high quality produce and we were able to get some amazing blueberries from here as well.

Lake Entiat Fruit stand: address 14360 US-97 ALT, Entiat, WA 98822 ; phone number (509) 393-0539 websiteFacebook We had some amazing strawberries out of here. Seriously, our car smelled delightful from the ride home. Matt also picked up marinated mushrooms which is hard to find.

Homestead Fruit Stand: address 7920 State Highway 97A, Wenatchee, WA 98801; phone number (509) 665-8243. They had some great produce and we were able to pull some ripe tomatoes. This is the first stand into Entiat from Wenatchee. They had a good selection of Lavender.

DeLap Fruit Stand: addressmilepost 275 Hwy 97 Malott, WA, United States, Washington 98829; phone number (509) 422-3145; Facebook page; They have some fruit that you may not have had before. You can find Apruims and Pluots. They have one of the dancing guys and are an easy stop off Hwy 97.

Estes Fruit Stand and Flowers: address 13656 US-2, East Wenatchee, WA 98802; phone (509)884-2034; Facebook page ; This was one of my mother’s favorites. They have this amazing flower selection and this was the earliest that that I spotted this year’s apples as they had some early varieties.

E & E Fruit Shack; address 4th St SE, East Wenatchee, 98802. There is no website or Facebook page. It is however right next to the family’s orchard. We were able to pick up some great plums, they also had peaches, and a bunch of zucchini. If you want to put money directly into a farmer’s hands then this is where you want to pick up fruit here at least once during the season.

Feil Pioneer Fruit Stand: 13083 US-2; East Wenatchee, WA 98802. Phone number 509-669-1754. This is right on the highway next to the round about. Great selection of fresh fruit. The earliest spot that we found Pears and Apples. They even had a great selection of tomatoes.

Prey’s Fruit Barn: 110007 Hwy 2, Leavenworth. Phone number 509-548-5771. Facebook pagewebpage This is right outside of Leavenworth with the large American Flag. They had a good assortment of fruit and are open year round. Very tourist friendly and we were able to pick up unusual sodas.

Bonus: The Local Granola: address 1408 Main Street Oroville, WA, United States, Washington 98844; phone number (509) 476-7037; webpageFacebook They offer a small natural foods selection. The Granola is worth the stop. We also got beard supplies.

Rules for fruit stand visits.

Bring cash. The smaller operations will appreciate you as they don’t have to make transaction fees.

Don’t be afraid to call ahead or ask if you don’t see something. It’s literally how I got Pie Cherries.

When you find one that is awesome then take a picture and share them on Facebook. Bonus points if you tag them so that more people can find them.

If we missed a favorite one then let us know in the comments.

At Wenatchee Insurance, we lend a hand to farms and orchards with a wide background. Insuring your family business can be tricky and adding crop insurance requires some skills. Some folks are looking for a Multi- Peril Crop Insurance where others are needing Whole Farm Revenue Protection. Living in the Apple Capital of the World, we have have run between the trees more than once.

We will ask questions so that we can get a better picture about your orchard or farm to make sure that you are not creating a coverage gap. For us, we believe that insurance should be:

Affordable. If you can not pay for it then it doesn’t make sense.

Understandable. This creates big problems if someone has something that they don’t know how it works.

Useable. If an emergency arises then we want you to be able to use it.

Crop insurance questions

What is the address of your orchard or farm?

What is the name of the orchard or farm?

Who has an interest in the orchard beyond yourself?

What is your and any other people with interest’s SSN?

What is the business’ EIN (If individual SSN or RAN is fine)

Are you leasing the orchard?

If so what is the % agreement?

What fruit or crop are you growing?

How many acres do you have of which crop?

What are the last 5 years of production? We will need it by block if possible

If new farmer can you procure the previous farmer’s records?

Are you tearing out any part of your orchard for next year? Or is there any new tree you think will produce this year?

Anything you think I should know?

What’s next to insure your crops?

After collecting the information, we go looking for coverage that covers your needs. What works for Farmer Fred’s potatoes in Quincy may completely miss Oliver Pear Orchard in Cashmere. Not everyone needs or can get crop insurance. We do our best to be responsive whether it is you talking or if you are sending your spouse.

When you are ready let’s talk. We have found that a conversation is a great way to begin.

At Wenatchee Insurance, we lend a hand to business owners with a wide background. Business insurance can be tricky. Some are just starting their journey where some have been running their family business for five generations. We even got involved with lending a hand with assisting Enterprise For Equity to help people better insure their business.

We will ask questions so that we can get a better picture about your business to make sure that you are not creating a coverage gap. For us, we believe that insurance should be:

Affordable. If you can not pay for it then it doesn’t make sense.

Understandable. This creates big problems if someone has something that they don’t know how it works.

Useable. If an emergency arises then we want you to be able to use it.

Retail business insurance questions

1) What is the official name of your business?

2) What is the address where you operate? Is it online only home based?

3) Do you have a different mailing address? If so What?

4) What is a your business phone #?

5) How much do you think you’re going to be making this year?

6) Does anyone else own a stake in the business?

7) Do you use your car to make deliveries?

8) What is the product/s you sell?

9) How many employees will you have?

10) Are there any additional insureds? (Landlords/owners)

11) Anything you think I should know?

What’s next to insure your business?

After collecting the information, we go looking for a good insurance company that fits your business. Some insurance companies may charge more or even not cover something that you need. What works for Farmer Fred in Quincy may completely miss Oliver Orchard in Cashmere. Not everyone needs crop insurance. The old company that your grandfather used may not cover the drones that you are using today.

When you are ready let’s talk. We have found that a conversation is a great way to begin.

In our area we have a select few dentists and orthodontists that accept Apple Health. When our son needed braces, every six weeks we would make the drive from Wenatchee to Ellensburg so that he would have his teeth worked on. It took a lot of coordination between his pediatric dentist and the orthodontist to get the approval.

Where to find Apple Health Dental care?

OK, have you been to the Dentist Link Set up by the Healthcare Authority? It provides an excellent search tool to find a dentist accepting Apple Health Dental in your area. You can also call or test a referral specialist 844-888-5465 from 8 am to 4:30 pm on weekdays.

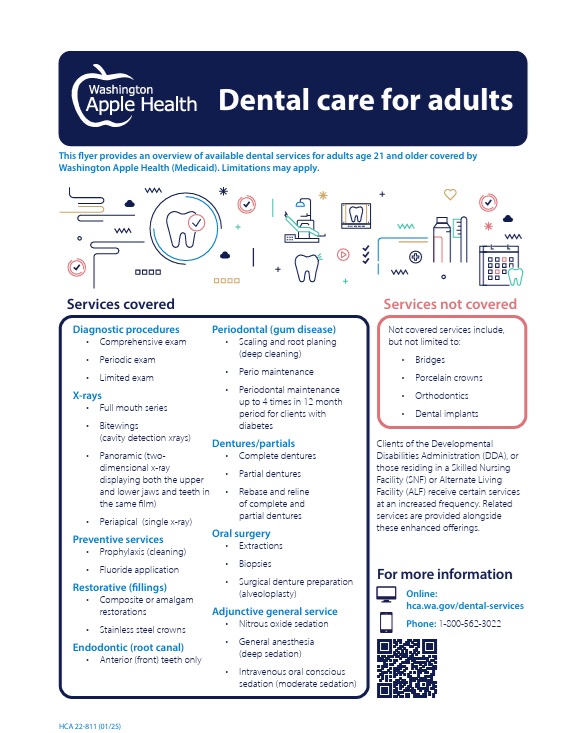

What does Apple Health Dental cover for adults?

If you have Apple Health as an adult it covers more than people think. Yes, it really does take care of fillings, front teeth root canals and dentures. There are some things that it doesn’t cover by it’s self like Dental Implants and Adult Orthodontics.

How do I enroll?

Suzie and Matt have been assisting people enroll for over a decade into Apple Health plans. We have never charged a fee and do not get paid for enrolling people in these plans. We do it because people in our community use healthcare and it is expensive to go without. There are no enrollment periods with Apple Health and it is based on our income level.

Children have expanded access to Apple Health using the Children’s Health Insurance Program (CHIP). Some will be zero cost or there will be a $20 or $30 monthly charge per child fee. We have a lot of families where the parents are on a paid health plan and the kids are on Apple Health. The important thing is that the family is being covered.

What happens if I am no longer eligible for Apple Health Dental

We have the conversation. We have access to several dental plans that a person can enroll year round. Some with waiting periods and some without. We even have plan that can assist adults with getting braces after a waiting period at Wenatchee Insurance. We make it as easy as possible to review your options.

There are times when it get’s incredibly busy for healthcare so you may have to wait a little bit longer in the Fall.

For Medicare the Annual Enrollment Period for Medicare Drug Plans and Medicare Advantage plans is October 15th through December 7th.

For Medicare’s Initial Enrollment it is three months before you turn 65, the month of your birthday and three months after.

For Healthcare the Open Enrollment Period is November 1st through December 15th. (some states may have an extension so do not hesitate to ask).

Yes, people set appointments early in the year for fall appointments to insure that they are able to have a conversation about the changes to their health plan.

The term “no-fault” in auto insurance can be confusing, especially if you’ve never had to file a claim. While it might sound like it removes responsibility, that’s not entirely accurate. Instead, no-fault insurance refers to how claims are handled after an accident, specifically, how medical bills and related expenses are paid, regardless of who caused the crash. Here’s an explanation from your insurance representative at Wenatchee Insurance Agency, serving Wenatchee, WA.

How No-Fault Insurance Works

In states that follow a no-fault system, each driver’s insurance policy covers their own policyholder’s medical expenses after an accident, up to a certain limit. This happens regardless of who was at fault. The primary goal of no-fault insurance is to reduce lawsuits related to minor accidents and ensure injured drivers receive treatment quickly.

Washington is not a traditional no-fault state, but drivers here have the option to add Personal Injury Protection (PIP) coverage to their policies. PIP functions similarly to no-fault insurance, covering medical expenses, lost wages, and essential services without waiting for a liability determination.

What No-Fault Insurance Does Not Cover

No-fault insurance does not cover damage to your vehicle or someone else’s property. These types of claims still require determining fault, with the at-fault driver’s liability coverage typically paying for repairs. Additionally, in serious accidents involving significant injuries, lawsuits may still be permitted—even in no-fault states—if damages exceed policy thresholds.

Know Your Options in Washington

Since no-fault insurance is optional in Washington, it’s important to review your policy and understand the level of protection you have. Adding PIP coverage can provide an extra layer of financial support if you’re injured, even if the other driver is uninsured. Your experienced local agent at Wenatchee Insurance Agency, serving Wenatchee, WA, can help you determine if this coverage is right for you. Contact us today to learn more.

One of the first people that Suzie enrolled was a refugee from Central America. It was an incredibly dangerous journey and they were needing medical attention to recover. Without Apple Health, they would not have received the care that they needed.

During Trump 1.0, Matt had a mom refuse to complete an application for their children over fear of the father being deported. That is a monstrous choice that no mother should have to make that he witnessed first hand. It’s why we are very protective of data and who we hand it over to.

Yes, some very cruel individuals like to threaten folks with public charge with all programs. It is important to note: The public charge rule will not consider any other federal or state benefits. That includes SNAP, WIC, CHIP, school lunches, Medicaid, Section 8 housing benefits, food banks, shelters, COVID-related medical care, and many more. So sometimes even we can not overcome fears on what will be used against families.

We can say that we have a couple of the insurance nerds at the office that used to ran one of the enrollment centers so we are real familiar with the Healthplanfinder for immigrants and the data that goes back and forth there. They don’t exchange medical data. There is a couple of Federal Hubs that they verify data with however those require the SSN.

The information is used for enrollment and states right on the front page it will not be used for immigration enforcement.

Medicaid falls under the Healthcare Authority’s control. If you don’t have access then here is a better description on what was taken.

The following programs were impacted by the breach:

Alien Emergency Medical

Apple Health Expansion

Civil Transitions

Non-Citizen Pregnant Women

Medicaid Family Planning (Take Charge)

The Alien Emergency Medical is a catastrophic program like dying of Cancer level patients. It’s one that no one wants to be on but delivers care to the patient and funds to the providers.

We don’t work directly with Civil Transitions, Non-Citizen Pregnant Women and Medicaid Family Planning as there are some programs that are not common on the Healthplanfinder.

Undocumented Immigrants make up about 24% of the uninsured in Washington State. Which is a priority to gain coverage to reduce the uninsured rate in the state.

At the office level, data is kept encrypted and not sold or shared expect to enroll people into insurance plans. We do everything in our power to prevent data breeches at a local level.

It is going to take the Legislatures at the STATE level to do something to prevent data from being stolen again.

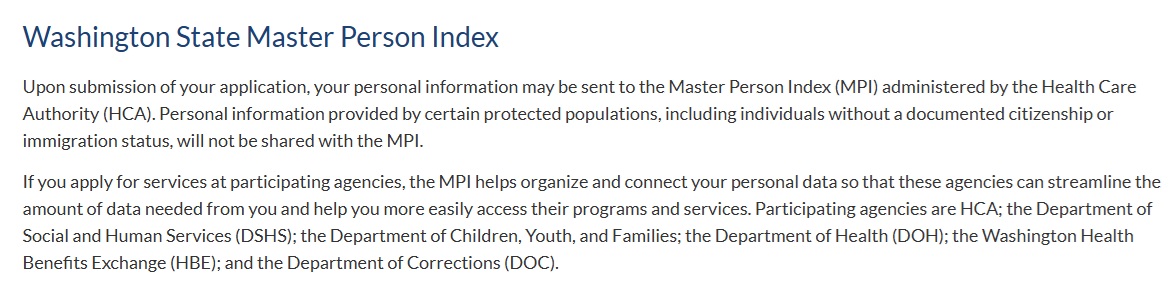

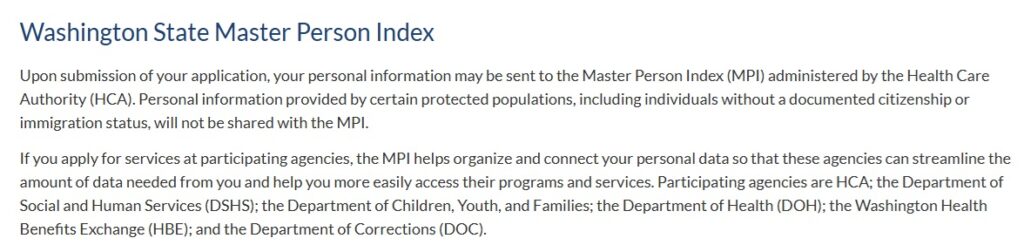

The Washington Healthplanfinder Privacy Notice talks about their commitment to Privacy and provides contact information if you would like further assistance. The Master Person Index (MPI) is administered by the Healthcare Authority. Here is their statement:

Healthplanfinder does send out 1095 forms for taxes

If you pay for your health insurance on the Washington Healthplanfinder then you must file your taxes every year. It is an IRS rule. Yes, regardless of your income level, you will always want to file your taxes. If your Uncle Fred says that you do not need to then look at what Uncle Sam has to say about the IRS rule.

During the first couple of weeks of the year a copy of a Form 1095-A is mailed out. If you can not find a your copy then let us know. Since the second year, we have been printing and email copies to our customers at no charge so that they could file their taxes.

(If you have Apple Health then you could receive a Form 1095-B. This form is not required to file your taxes and you can request a new copy from the Healthcare Authority. )

When you file your taxes, you take the information from your 1095-A and reconcile it using the IRS Form 8962. It involves comparing the amount of premium tax credits used with the eligible amount, based on final annual income. This is why you want your income on the Washington Healthplanfinder as accurate as possible and you can updated it during the year if your income changes.

The Advanced Premium Tax Credits are what is used to lower your monthly cost of health insurance. It is an advance so if you underestimate your income then you will be asked to pay back the portion that was advanced to you. The reverse is true if you over-estimate your income while you will pay more monthly for health insurance then you will also be paid back any unused tax credits.

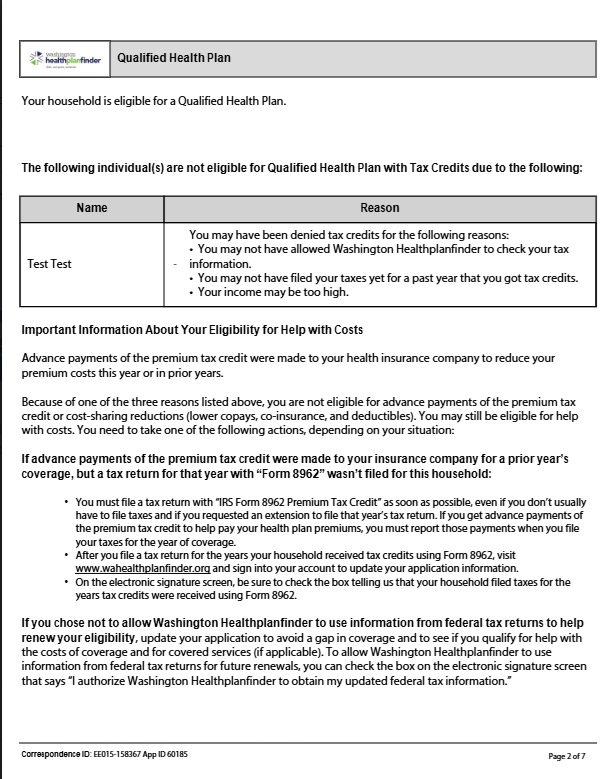

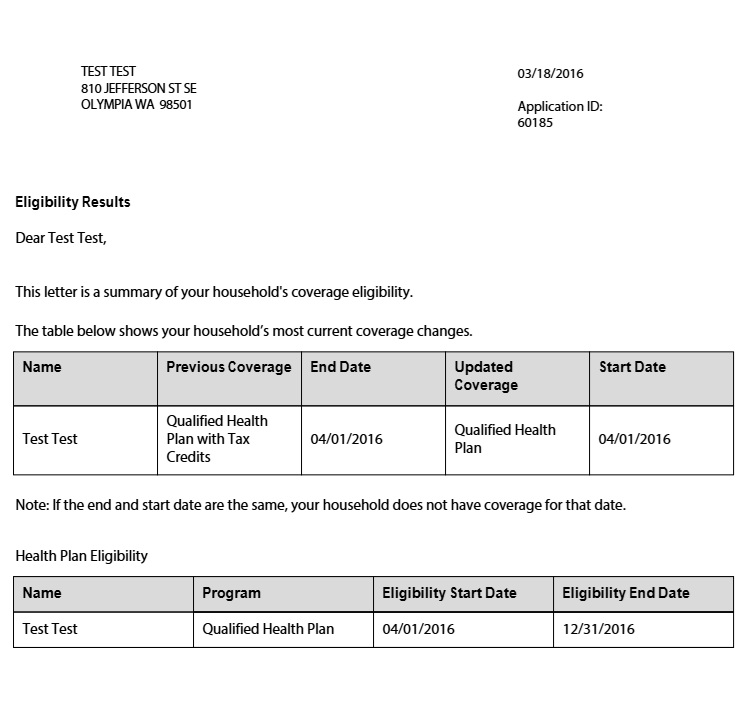

Some reasons you could lose the Advanced Premium Tax Credits because:

You did not file taxes and reconcile tax credits from previous years.

Did not consent on application for the Washington Healthplanfinder to request updated tax information.

Customers who are married filing single instead of jointly on their tax return.

If you lose the Advanced Premium Tax Credits then suddenly what you are required to pay for health insurance can increase!

You could receive a letter you don’t understand otherwise known as the scary letter that looks like this:

If you get a scary letter an want help then give Suzie or Matt a call at Wenatchee Insurance. We can confirm what the situation is and how to correct it. This is insurance so it does take times to make changes and it is one of the reasons that we recommend filing taxes as early as possible to reduce problems with your advanced premium tax credits.

Open Enrollment for the Washington Healthplanfinder is November 1 through December 15.

Let’s talk about the least exciting calendar dates you’ll ever mark with a glitter pen—health insurance and Medicare enrollment deadlines. But just because they don’t come with cake or party hats doesn’t mean they’re not important. Miss the window, and you might end up paying more than your fair share (or going without coverage—yikes!). Luckily, Suzie from Wenatchee Insurance has your back, clipboard in hand, ready to keep you on track across North Central Washington.

Health Insurance Enrollment (AKA: Don’t Snooze, or You’ll Lose)

If you’re under 65 and buying your health insurance through the Washington Healthplanfinder, here’s what you need to know:

Open Enrollment: November 1 – December 15 This is the biggie. You can sign up, switch plans, or renew your current coverage. Want to ring in the New Year without a health insurance hangover? Select an appointment early as this is the shortest enrollment ever in Washington State!

Special Enrollment Periods (SEP): Life happens—marriages, babies, losing job-based insurance, moving, or even getting out of jail (yes, that’s a legit trigger). These events may qualify you for a 60-day SEP.

Suzie’s advice: “If you’re not sure whether your life change qualifies, give me a call. I love solving insurance mysteries more than I love huckleberry pie. And I really love huckleberry pie.”

If you or a loved one is turning 65, you’ve got your own enrollment clock ticking. Medicare has its own little maze of dates, but Suzie knows the shortcuts.

Initial Enrollment Period (IEP): Starts 3 months before you turn 65, includes your birthday month, and goes 3 months after. That’s a 7-month window to get into Medicare Part A and Part B.

Medicare Advantage & Drug Plans (Part C & D) Annual Enrollment: October 15 – December 7 This is the time to change, drop, or add Medicare Advantage or Prescription Drug Plans. Your changes kick in January 1.

Medicare Advantage Open Enrollment Period: January 1 – March 31 Didn’t love your Medicare Advantage plan after New Year’s? You get one switch during this time.

Suzie’s tip: “Don’t wait until December 6 to call me. I’ll be caffeinated, but it’s best to chat while we’re both relaxed and not trying to understand Medicare with Christmas music blasting in the background.”

Native American Health and Apple Health

These applications have year round enrollments. Apple Health is Washington State’s Medicaid program that we have a special information site set up for. If you have a Tribal Affiliation then yes, you can enroll every month of the year. It is why we run applications year round.

Navigating enrollment periods in Washington state is like trying to find a parking spot at Pybus Market on a Saturday morning—possible, but easier with a little help. Suzie doesn’t just know the dates, she knows the plans, the fine print, and where to find extra savings or better networks across North Central Washington.

Call Suzie at Wenatchee Insurance before your deadline becomes a dead-end. She’ll make sure you’re covered, confident, and maybe even chuckling through the paperwork.

Accidents happen. The rain falls, the wind blows, ice forms unexpectedly, or someone simply trips over their own feet. Regardless of the cause, someone was injured on your business premises, and they want you to cover their medical expenses. As a business owner, you have a “duty of care,” meaning you have a responsibility to ensure there is nothing on your property that could harm a potential customer. But as the saying goes, “stuff happens.” Fortunately, this is why you have Commercial Insurance.

What to Do if Someone Is Injured on Your Property

First and foremost, you must attend to the customer’s well-being. Call 911, describe the incident, follow the operator’s instructions, and wait for the paramedics to arrive. Even if you’re unsure, it’s better to call an ambulance. Apply necessary first aid. If the customer refuses an ambulance or the injuries aren’t serious, at least provide them a quiet place to rest and offer ice or a glass of water. Then, you must address the hazard. Block it off if necessary. Document the scene with pictures before you alter anything. Do not admit or imply anyone is to blame. Complete an incident report with the time and date of the accident. Collect statements from witnesses and the injured customer. Save any surveillance footage you may have. Once all of this is covered, you should contact your insurer as soon as possible.

Many types of Commercial Insurance

Commercial Insurance has been more than basic liability for years. Sometimes you need a business owners’ policy that can cover employee theft. Sometimes you need liquor liability, a bond, commercial auto, insuring your equipment on the job site for theft or completed goods. We like to have conversations so that if there is a claim that you understand your coverages better before you need them.

Contact Wenatchee Insurance Agency in Wenatchee, WA

If you are in the Wenatchee, WA area and need commercial insurance, please contact Wenatchee Insurance Agency. We’re here to help.

For nearly a decade we have assisted with Health & Medicare Solutions. We are proud to be selected by the Washington Healthplanfinder to be one of ten Enrollment Centers located in Washington State.